Control depends on accurate records, disciplined processes, and lifecycle management

Most organisations believe they have control. They maintain asset registers, manage inventory within their systems, and report financial values through the profit and loss (P&L). The structure is in place, the systems are live, and the reports are produced regularly. On the surface, everything appears to be working.

The reality is often very different. Asset registers do not reflect what is physically held or the condition of those assets. Inventory records do not align with what can actually be used, sold, or supported. Financial reporting continues to carry values that no longer represent operational reality. Each function operates within its own structure, often in, using its own data, and the gaps between them are rarely addressed.

This is where control is lost. Decisions are made using data that looks correct but does not reflect what is happening across the supply chain. The impact is not immediate, which is why it is often missed. It builds over time through excess, slow-moving, and forgotten inventory, inaccurate asset records, and financial exposure that is not fully understood. By the time the issue becomes visible, it is no longer a data problem. It is a failure of control.

Control depends on accurate records and disciplined processes

Asset management depends on accurate records. Asset registers, inventory systems, and financial data provide the information needed to understand what assets exist, where they are, what condition they are in, and what value they represent. Without this, there is no reliable basis for decision making.

However, records alone do not create control. They must be supported by defined and consistently applied processes. Data must be maintained, validated, and aligned across functions. Operational activity, inventory management, and financial reporting must be connected so that decisions are made using the same information.

ISO 55000 defines asset management as the coordinated activity of an organisation to realise value from its assets. That coordination only happens when records, processes, and decisions are aligned. Without it, organisations collect data but fail to use it in a way that delivers control or value.

In practice, this means organisations must move beyond maintaining systems and focus on how information flows between functions. Asset data must be updated as conditions change. Inventory must reflect what is usable and relevant. Financial reporting must reflect what can realistically be realised. When these elements are connected through process, control becomes possible.

If lifecycle is not understood, problems will follow

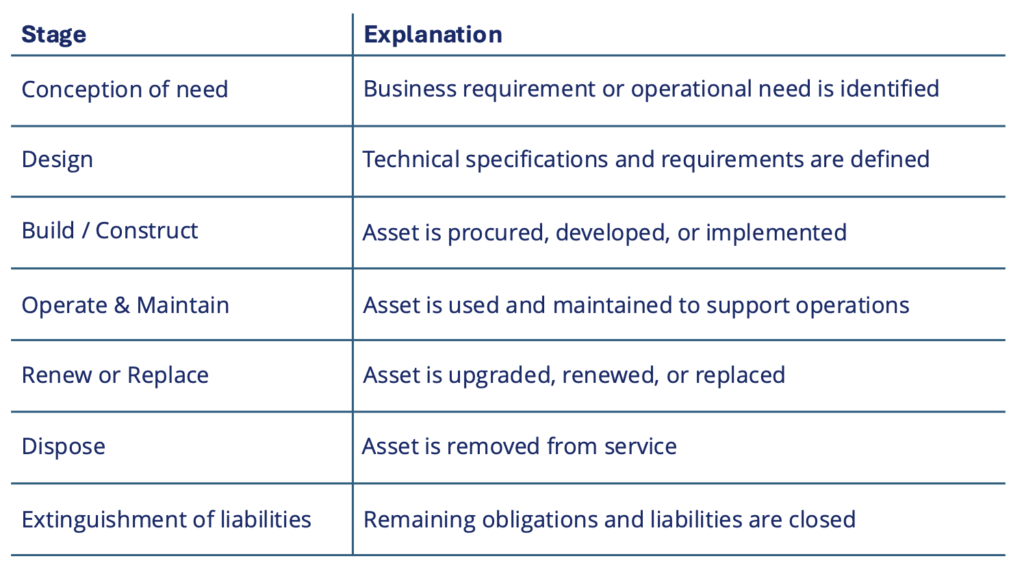

Assets move through a lifecycle, and every stage requires different decisions, controls, and behaviours. ISO 55000 defines this lifecycle from the initial need through to disposal and the removal of obligations. This is not a theoretical model. It is the structure required to manage assets in a controlled and consistent way.

In practice, organisations must actively manage assets through key stages:

- Planning and defining the need based on organisational objectives

- Acquisition and introduction into the organisation

- Operation and maintenance to deliver required performance

- Review, renewal, or replacement based on cost, risk, and performance

- Disposal and closure, including the removal of liabilities

When this lifecycle is not understood or applied, problems begin to build. Inventory continues to be purchased without regard to declining demand. Assets remain active in systems long after they have stopped delivering value. Financial values continue to be reported based on outdated assumptions. The organisation slowly loses alignment between what exists, what is needed, and what is being reported.

Lifecycle management provides the structure to prevent this. It ensures that decisions are made at the right time, using the right information, and aligned to the actual state of the asset.

End of life is where most organisations fail

The end-of-life stage is where control is most often lost. Assets that no longer deliver value remain on registers. Inventory that no longer supports demand continues to be held. Financial values are carried forward even when they no longer reflect what can be realised.

This creates a slow accumulation of risk. Excess, slow-moving, and forgotten inventory builds across the organisation. Asset registers become unreliable. Financial reporting becomes increasingly disconnected from operational reality. When action is finally taken, it is often reactive, large in scale, and financially disruptive.

Control at this stage requires clear and consistent processes. Organisations must regularly assess asset condition, relevance, and performance. They must define when an asset or inventory item no longer supports operational or commercial objectives. Decisions must be made on whether to retain, redeploy, repurpose, or remove. Disposal and write-off processes must be clearly defined, controlled, and aligned with financial reporting.

Typical triggers for action include declining demand, rising holding costs, changes in regulatory requirements, or the introduction of replacement assets. When these triggers are recognised early and acted on, organisations maintain control. When they are ignored, problems build in the background.

Asset management is not complete until assets are properly exited and records reflect that reality.

Without structure, control is inconsistent

Asset management cannot rely on individual decisions or isolated processes. It requires structure. ISO 55000 introduces the concept of an asset management system, which provides the framework needed to manage assets consistently across the organisation.

Recurring issues highlight where decisions are not aligned with actual demand, where processes are not functioning as intended, and where assumptions are not being challenged. These patterns provide valuable insight into how the system is operating. Ignoring them allows the behaviour to continue unchecked, reinforcing the cycle rather than breaking it.

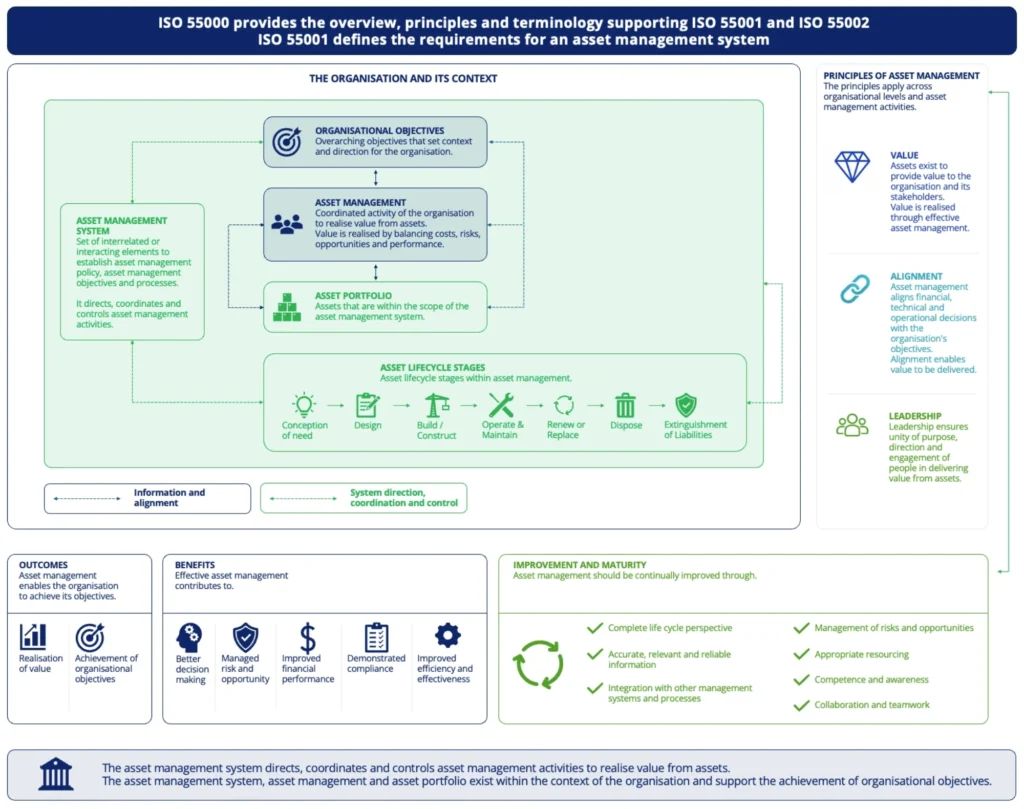

The ISO 55000 asset management framework in practice

The ISO 55000 framework brings structure to asset management by connecting organisational objectives, asset management activities, lifecycle thinking, and decision making into a single, aligned system. It is not a process to follow, but a model that shows how control is created when data, processes, and decisions work together.

ISO 55000:2024 Asset management – Vocabulary, overview and principles

Explanation of the ISO 55000 asset management structure

1. Organisational objectives

Purpose

Defines the strategic direction and priorities of the organisation.

Focus areas

- Operational performance

- Risk reduction

- Reliability and availability

- Compliance and governance

- Growth and sustainability

Why it matters

Asset management activities should align with organisational objectives to ensure assets support business goals and long-term value.

2. Asset management

Definition

Coordinated activity of the organisation to realise value from assets.

Core balance

- Cost

- Risk

- Opportunity

- Performance

Why it matters

Asset management ensures assets continue to deliver operational, financial, and strategic value throughout their lifecycle.

3. Asset portfolio

Purpose

Defines the assets that fall within the scope of the asset management system.

Examples

- Offshore equipment

- Operational assets

- Warehoused inventory

- Infrastructure

- Vessels and machinery

Why it matters

Organisations require visibility, control, and understanding of asset condition, utilisation, and risk exposure.

4. Asset lifecycle stages

Lifecycle approach

ISO 55000 applies asset management across the full asset lifecycle.

Why it matters

Lifecycle management supports long term decision making, cost control, sustainability, and operational reliability.

5. Asset management system

Purpose

Provides the structure used to direct, coordinate, and control asset management activities.

Includes

- Policies

- Objectives

- Governance

- Processes

- Compliance

- Reporting

- Roles and responsibilities

Why it matters

The asset management system creates consistency, accountability, and repeatability across the organisation.

6. Principles of asset management

Value

Assets exist to provide value to the organisation and its stakeholders. Effective asset management ensures value is realised through informed and balanced decision making.

Alignment

Asset management aligns financial, operational, and technical decisions with organisational objectives. Alignment ensures all functions support common business goals.

Leadership

Leadership establishes direction, accountability, and engagement. Strong leadership supports consistency, governance, and organisational culture.

7. Outcomes

Asset management enables organisations to achieve:

- Improved operational performance

- Increased reliability

- Better availability

- Reduced downtime

- Improved asset utilisation

Why it matters

The objective of asset management is to support the achievement of organisational objectives and the realisation of value.

8. Benefits

Benefits of effective asset management

- Better decision making

- Managed risk and opportunity

- Improved financial performance

- Demonstrated compliance

- Improved efficiency and effectiveness

Why it matters

Effective asset management supports stronger governance, improved performance, and long-term sustainability.

9. Improvement and maturity

Continual improvement includes:

- Complete lifecycle thinking

- Accurate and reliable information

- Integration with management systems

- Risk and opportunity management

- Appropriate resourcing

- Competence and awareness

- Collaboration and teamwork

Why it matters

Organisations mature asset management capability through continual improvement of systems, processes, governance,

and decision making.

Conclusion

ISO 55000 establishes the principles, terminology, and overall structure of asset management.

It provides organisations with a consistent and value driven approach to managing assets, supporting operational performance, governance, risk management, and strategic alignment.

ISO 55001 builds on these principles by defining the formal requirements for implementing an auditable asset management system.

Compliance does not create control

Many organisations place significant focus on compliance. Regulatory requirements, controlled equipment standards, and audit processes are introduced to demonstrate that assets are being managed correctly.

Compliance is necessary, particularly where safety, environmental, or legal obligations exist. However, compliance does not guarantee control. It is possible to meet regulatory requirements while still operating with inaccurate data, disconnected systems, and poor decision making.

ISO 55000 provides the principles that underpin effective asset management, including value, alignment, and leadership. These principles must be applied in practice. Processes must be followed, data must be accurate, and decisions must be aligned across the organisation. When this happens, compliance becomes a natural outcome of good asset management.

When it does not, compliance becomes a separate activity that adds effort but does not improve control.

If the data is wrong, the decisions will be wrong

Asset management relies on data and information to support decision making. When asset data, inventory records, and financial reporting are not aligned, the information used for decisions becomes unreliable.

Inventory may be recorded as available when it is not usable. Assets may be listed as active when they no longer perform. Financial values may reflect historic assumptions rather than current conditions. These inconsistencies affect planning, procurement, maintenance, and financial decisions.

The result is predictable. Decisions are made based on assumptions rather than reality. Risk increases. Performance becomes difficult to measure. Confidence in the data begins to decline.

Reliable decisions require reliable information. Alignment across asset data, inventory, and financial reporting ensures that decisions are based on what actually exists, not what systems suggest.

Final though

Asset management, inventory, and financial reporting are different views of the same assets. When they are aligned, organisations operate with clarity. They understand what they have, what it is worth, and how it supports the business. Decisions are made with confidence, and performance can be measured accurately.

When they are not aligned, the organisation operates in fragments. Inventory builds without purpose. Assets remain on registers without value. Financial reporting reflects assumptions rather than reality. The organisation spends its time reacting to problems rather than controlling them.

ISO 55000 makes it clear that asset management is a coordinated activity designed to realise value. That coordination does not come from systems alone. It comes from accurate records, structured processes, lifecycle discipline, and alignment across functions.

This is not a reporting issue. It is not a system issue. It is a discipline issue.

Organisations that get this right do not just manage assets. They control them.